Is An Owner's Draw Retained Earnings

Corporation Bookkeeping

86 Compare and Contrast Owners' Equity versus Retained Earnings

Owners' equity represents the business owners' share of the company. It is oft referred to every bit net worth or net assets in the financial world and as stockholders' equity or shareholders' equity when discussing businesses operations of corporations. From a practical perspective, it represents everything a company owns (the company's assets) minus all the company owes (its liabilities). While "owners' disinterestedness" is used for all three types of business organizations (corporations, partnerships, and sole proprietorships), only sole proprietorships name the balance sheet account "owner's equity" as the unabridged equity of the company belongs to the sole owner. Partnerships (to be covered more thoroughly in Partnership Accounting) oft characterization this section of their balance sheet equally "partners' equity." All three forms of business utilize different bookkeeping for the respective equity transactions and employ different equity accounts, but they all rely on the same relationship represented by the bones accounting equation ((Figure)).

Accounting Equation. The relationship among assets, liabilities, and disinterestedness is represented in the bookkeeping equation. (attribution: Copyright Rice University, OpenStax, under CC Past-NC-SA iv.0 license)

Three Forms of Business Ownership

Businesses operate in one of three forms—sole proprietorships, partnerships, or corporations. Sole proprietorships utilize a single account in owners' equity in which the possessor'southward investments and net income of the company are accumulated and distributions to the owner are withdrawn. Partnerships utilize a split up majuscule business relationship for each partner, with each capital business relationship property the corresponding partner'southward investments and the partner's corresponding share of cyberspace income, with reductions for the distributions to the respective partners. Corporations differ from sole proprietorships and partnerships in that their operations are more than complex, ofttimes due to size. Unlike these other entity forms, owners of a corporation usually change continuously.

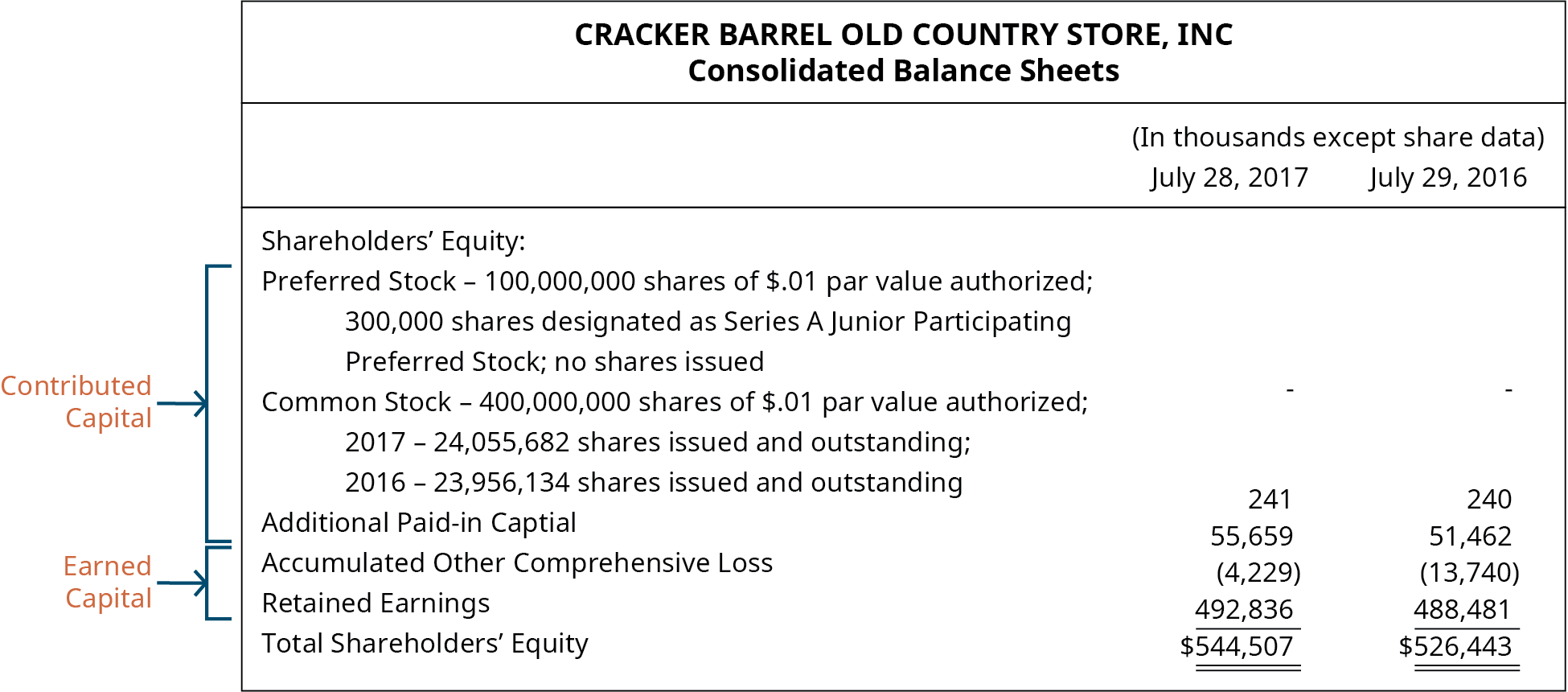

The stockholders' equity section of the balance sail for corporations contains two chief categories of accounts. The first is paid-in capital, or contributed capital—consisting of amounts paid in by owners. The 2d category is earned capital, consisting of amounts earned by the corporation every bit office of business operations. On the balance sail, retained earnings is a key component of the earned capital section, while the stock accounts such as mutual stock, preferred stock, and additional paid-in capital are the chief components of the contributed capital section.

Contributed Capital letter and Earned Capital

The stockholders' disinterestedness department of Cracker Butt Old Land Shop, Inc.'s consolidated residuum sheet as of July 28, 2022, and July 29, 2022, shows the company'due south contributed capital and the earned uppercase accounts.1

Characteristics and Functions of the Retained Earnings Business relationship

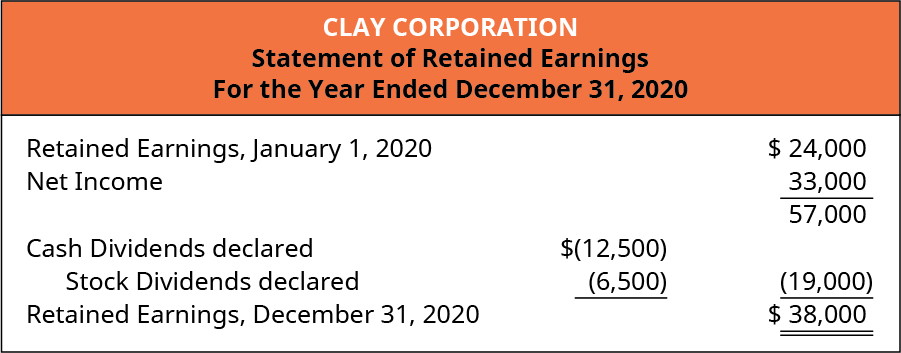

Retained earnings is the primary component of a company'southward earned capital. It generally consists of the cumulative net income minus any cumulative losses less dividends declared. A bones statement of retained earnings is referred to as an analysis of retained earnings considering information technology shows the changes in the retained earnings account during the period. A company preparing a full set of financial statements may choose between preparing a statement of retained earnings, if the activity in its stock accounts is negligible, or a argument of stockholders' disinterestedness, for corporations with activeness in their stock accounts. A statement of retained earnings for Clay Corporation for its second year of operations ((Figure)) shows the company generated more net income than the corporeality of dividends it declared.

Statement of Retained Earnings for Clay Corporation. (attribution: Copyright Rice University, OpenStax, under CC By-NC-SA iv.0 license)

When the retained earnings balance drops below goose egg, this negative or debit balance is referred to as a deficit in retained earnings.

Restrictions to Retained Earnings

Retained earnings is oftentimes subject area to certain restrictions. Restricted retained earnings is the portion of a company's earnings that has been designated for a detail purpose due to legal or contractual obligations. Some of the restrictions reflect the laws of the state in which a company operates. Many states restrict retained earnings by the cost of treasury stock, which prevents the legal capital of the stock from dropping below nil. Other restrictions are contractual, such every bit debt covenants and loan arrangements; these exist to protect creditors, frequently limiting the payment of dividends to maintain a minimum level of earned capital.

Appropriations of Retained Earnings

A company's board of directors may designate a portion of a visitor's retained earnings for a item purpose such every bit future expansion, special projects, or as office of a company'due south chance direction programme. The amount designated for a particular purpose is classified equally appropriated retained earnings.

There are two options in accounting for appropriated retained earnings, both of which allow the corporation to inform the fiscal statement users of the company's hereafter plans. The first accounting option is to brand no journal entry and disclose the amount of cribbing in the notes to the financial statement. The 2nd option is to record a periodical entry that transfers part of the unappropriated retained earnings into an Appropriated Retained Earnings business relationship. To illustrate, assume that on March 3, Clay Corporation's board of directors appropriates $12,000 of its retained earnings for future expansion. The company'due south retained earnings account is first renamed every bit Unappropriated Retained Earnings. The periodical entry decreases the Unappropriated Retained Earnings account with a debit and increases the Appropriated Retained Earnings account with a credit for $12,000.

The company will written report the advisable retained earnings in the earned uppercase section of its residual sheet. It should be noted that an appropriation does not set aside funds nor designate an income statement, nugget, or liability effect for the appropriated amount. The appropriation simply designates a portion of the company'due south retained earnings for a specific purpose, while signaling that the earnings are existence retained in the company and are not available for dividend distributions.

Statement of Stockholders' Disinterestedness

The statement of retained earnings is a subsection of the statement of stockholders' equity. While the retained earnings statement shows the changes betwixt the beginning and ending balances of the retained earnings business relationship during the period, the statement of stockholders' equity provides the changes between the first and ending balances of each of the stockholders' equity accounts, including retained earnings. The format typically displays a separate column for each stockholders' disinterestedness account, every bit shown for Clay Corporation in (Effigy). The central events that occurred during the twelvemonth—including net income, stock issuances, and dividends—are listed vertically. The stockholders' equity section of the company's residuum sheet displays only the ending balances of the accounts and does non provide the action or changes during the period.

Argument of Stockholders' Equity for Clay Corporation. (attribution: Copyright Rice University, OpenStax, under CC Past-NC-SA 4.0 license)

Nigh all public companies written report a statement of stockholders' equity rather than a argument of retained earnings because GAAP requires disclosure of the changes in stockholders' disinterestedness accounts during each bookkeeping catamenia. Information technology is significantly easier to encounter the changes in the accounts on a argument of stockholders' equity rather than equally a paragraph notation to the financial statements.

Corporate Accounting and IFRS

Both U.S. GAAP and IFRS require the reporting of the various owners' accounts. Under U.S. GAAP, these accounts are presented in a statement that is most oftentimes called the Statement of Stockholders' Equity. Under IFRS, this statement is usually called the Argument of Changes in Equity. Some of the biggest differences between U.S. GAAP and IFRS that arise in reporting the various accounts that appear in those statements chronicle to either categorization or terminology differences.

U.S. GAAP divides owners' accounts into 2 categories: contributed upper-case letter and retained earnings. IFRS uses three categories: share capital, accumulated profits and losses, and reserves. The first two IFRS categories correspond to the two categories used under U.S. GAAP. What about the tertiary category, reserves? Reserves is a category that is used to written report items such every bit revaluation surpluses from revaluing long-term avails (see the Long-Term Assets Feature Box: IFRS Connexion for details), as well as other equity transactions such as unrealized gains and losses on available-for-sale securities and transactions that fall under Other Comprehensive Income (topics typically covered in more avant-garde accounting classes). U.South. GAAP does not use the term "reserves" for any reporting.

There are also differences in terminology between U.S. GAAP and IFRS shown in (Figure).

| Terminology Differences betwixt U.South. GAAP and IFRS | |

|---|---|

| U.Due south. GAAP | IFRS |

| Common stock | Share capital |

| Preferred stock | Preference shares |

| Additional paid-in capital | Share premium |

| Stockholders | Shareholders |

| Retained earnings | Retained profits or accumulated profits |

| Retained earnings deficit | Accumulated losses |

All of this information pertains to publicly traded corporations, only what about corporations that are not publicly traded? Well-nigh corporations in the U.Due south. are not publicly traded, so do these corporations use U.S. GAAP? Some do; some do not. A non-public corporation can use cash basis, tax basis, or full accrual basis of accounting. Virtually corporations would utilise a full accrual basis of accounting such as U.Due south. GAAP. Cash and tax basis are most likely used but by sole proprietors or small partnerships.

However, U.Southward. GAAP is not the simply full accrual method available to non-public corporations. Two alternatives are IFRS and a simpler course of IFRS, known as IFRS for Small and Medium Sized Entities, or SMEs for short. In 2008, the AICPA recognized the IASB every bit a standard setter of acceptable GAAP and designated IFRS and IFRS for SMEs equally an acceptable set of mostly accepted accounting principles. However, it is upward to each State Board of Accountancy to make up one's mind if that state will allow the utilize of IFRS or IFRS for SMEs by non-public entities incorporated in that land.

What is a SME? Despite the utilize of size descriptors in the title, qualifying as a pocket-sized or medium-sized entity has nada to do with size. A SME is any entity that publishes full general purpose financial statements for public use but does not have public accountability. In other words, the entity is not publicly traded. In addition, the entity, even if information technology is a partnership, cannot human activity as a fiduciary; for example, it cannot be a bank or insurance visitor and apply SME rules.

Why might a non-public corporation want to use IFRS for SMEs? Outset, IFRS for SMEs contains fewer and simpler standards. IFRS for SMEs has only nigh 300 pages of requirements, whereas regular IFRS is over 2,500 pages and U.S. GAAP is over 25,000 pages. Second, IFRS for SMEs is but modified every three years. This means entities using IFRS for SMEs don't take to oft adjust their bookkeeping systems and reporting to new standards, whereas U.S. GAAP and IFRS are modified more frequently. Finally, if a corporation transacts business with international businesses, or hopes to attract international partners, seek capital from international sources, or be bought out by an international company, and then having their fiscal statements in IFRS form would make these transactions easier.

Prior Menstruum Adjustments

Prior catamenia adjustments are corrections of errors that appeared on previous periods' financial statements. These errors can stalk from mathematical errors, misinterpretation of GAAP, or a misunderstanding of facts at the time the fiscal statements were prepared. Many errors impact the retained earnings business relationship whose balance is carried forrard from the previous period. Since the financial statements have already been issued, they must be corrected. The correction involves changing the fiscal statement amounts to the amounts they would accept been had no errors occurred, a process known equally restatement. The correction may impact both balance sheet and income statement accounts, requiring the visitor to record a transaction that corrects both. Since income statement accounts are closed at the terminate of every menstruum, the journal entry will contain an entry to the Retained Earnings account. As such, prior period adjustments are reported on a company's statement of retained earnings as an adjustment to the beginning remainder of retained earnings. By directly adjusting starting time retained earnings, the adjustment has no consequence on current menstruum net income. The goal is to separate the error correction from the electric current menstruation's net income to avoid distorting the current period'southward profitability. In other words, prior period adjustments are a way to go back and correct past financial statements that were misstated because of a reporting error.

Are Companies Making Fewer Errors in Fiscal Reporting?

According to Kevin LaCroix, additional reporting requirements created by the Sarbanes Oxley Deed prompted a surge in 2005 and 2006 of the number of companies that had to make corrections and reissue fiscal statements. Still, since that time, the number of companies making corrections has dropped over 60%, partially due to the number of U.South. companies listed on stock exchanges, and partially due to tighter regulations. The severity of the errors that acquired restatements has declined as well, primarily due to tighter regulation, which has forced companies to improve their internal controls.2

To illustrate how to correct an error requiring a prior period adjustment, assume that in early 2022, Clay Corporation'south controller determined it had made an error when calculating depreciation in the preceding yr, resulting in an understatement of depreciation of $1,000. The entry to correct the error contains a decrease to Retained Earnings on the argument of retained earnings for $1,000. Depreciation expense would take been $1,000 higher if the correct depreciation had been recorded. The entry to Retained Earnings adds an additional debit to the full debits that were previously part of the closing entry for the previous year. The credit is to the balance sail account in which the $1,000 would take been recorded had the right depreciation entry occurred, in this case, Accumulated Depreciation.

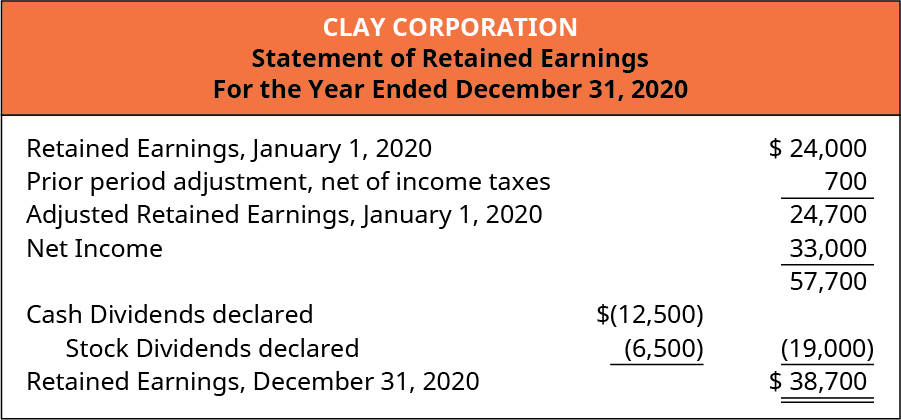

Because the adjustment to retained earnings is due to an income statement amount that was recorded incorrectly, there will also be an income tax result. The tax effect is shown in the argument of retained earnings in presenting the prior period aligning. Assuming that Clay Corporation's income tax rate is 30%, the tax outcome of the $1,000 is a $300 (xxx% × $1,000) reduction in income taxes. The increase in expenses in the amount of $1,000 combined with the $300 decrease in income revenue enhancement expense results in a net $700 decrease in net income for the prior period. The $700 prior menses correction is reported as an adjustment to beginning retained earnings, net of income taxes, equally shown in (Figure).

Statement of Retained Earnings for Clay Corporation. (attribution: Copyright Rice University, OpenStax, nether CC By-NC-SA 4.0 license)

Generally accepted bookkeeping principles (GAAP), the set up of accounting rules that companies are required to follow for financial reporting, requires companies to disclose in the notes to the financial statements the nature of whatsoever prior period adjustment and the related impact on the financial statement amounts.

The correction of errors in financial statements is a complicated state of affairs. Both shareholders and investors tend to view these with deep suspicion. Many believe corporations are attempting to smooth earnings, hide possible problems, or encompass up mistakes. The Journal of Accountancy, a journal published by the AICPA, offers guidance in how to manage this process. Scan the Periodical of Accountancy website for manufactures and cases of prior period adjustment issues.

Tune into Financial News

Tune into a financial news plan like Squawk Box or Mad Coin on CNBC or Bloomberg's. Notice the terminology used to draw the corporations beingness analyzed. Notice the speed at which topics are discussed. Are these shows for the novice investor? How could this information bear on potential investors?

Log onto the Annual Reports website to access a comprehensive collection of more than than 5,000 annual reports produced past publicly-traded companies. The site is a tremendous resource for both school and investment-related research. Reading annual reports provides a different type of insight into corporations. Beyond the financial statements, annual reports give shareholders and the public a glimpse into the operations, mission, and charitable giving of a corporation.

Key Concepts and Summary

- Owner'southward equity reflects an owner's investment value in a visitor.

- The iii forms of business organization employ different accounts and transactions relative to owners' equity.

- Retained earnings is the primary component of a company's earned majuscule. It generally consists of the cumulative net income minus any cumulative losses less dividends declared. A statement of retained earnings shows the changes in the retained earnings business relationship during the menstruation.

- Restricted retained earnings is the portion of a visitor'due south earnings that has been designated for a detail purpose due to legal or contractual obligations.

- A company'south board of directors may designate a portion of a company's retained earnings for a particular purpose such as future expansion, special projects, or as part of a company's chance management plan. The amount designated is classified as appropriated retained earnings.

- The argument of stockholders' disinterestedness provides the changes between the beginning and ending balances of each of the stockholders' equity accounts, including retained earnings.

- Prior period adjustments are corrections of errors that occurred on previous periods' fiscal statements. They are reported on a visitor's statement of retained earnings as an aligning to the beginning residue.

Multiple Choice

(Figure)Stockholders' equity consists of which of the following?

- bonds payable

- retained earnings and accounts receivable

- retained earnings and paid-in capital

- discounts and premiums on bond payable

(Figure)Retained earnings is accurately described by all except which of the following statements?

- Retained earnings is the chief component of a company's earned majuscule.

- Dividends declared are added to retained earnings.

- Cyberspace income is added to retained earnings.

- Net losses are accumulated in the retained earnings account.

(Figure)If a company'south board of directors designates a portion of earnings for a particular purpose due to legal or contractual obligations, they are designated as ________.

- retained earnings payable

- appropriated retained earnings

- cumulative retained earnings

- restricted retained earnings

(Figure)Corrections of errors that occurred on a previous menstruum'south fiscal statements are called ________.

- restrictions

- deficits

- prior menses adjustments

- restatements

(Figure)Owner's disinterestedness represents which of the following?

- the amount of funding the visitor has from issuing bonds

- the sum of the retained earnings and accounts receivable account balances

- the total of retained earnings plus paid-in capital

- the business possessor's/owners' share of the company, also known equally cyberspace worth or net avails

Questions

(Effigy)Your friend has questions near retained earnings and dividends. How do you explain to him that dividends are paid out of retained earnings?

(Figure)What does owners' equity mean for the owner?

Owners' equity is the value of assets in a visitor that remains after liabilities are fulfilled. Information technology is also referred to equally net worth or net assets.

(Effigy)What types of transactions reduce owner's equity? What types of transactions reduce retained earnings? What practise they have in common?

(Figure)Sometimes financial statements contain errors. What type of liabilities may need correction every bit a prior period adjustment?

An example would be the omission of a payroll accrual or a warranty estimate.

(Figure)Retained earnings may be restricted or appropriated. Explicate the difference between the two and give an example of when each may be used.

Exercise Prepare A

(Figure)Coating Visitor has paid quarterly dividends every quarter for the by fifteen years. Lately, slowing sales have created a cash crisis for the company. While the company still has positive retained earnings, the retained earnings rest is shut to zero. Should the company borrow to continue to pay dividends? Why or why non?

(Figure)Farmington Corporation began the year with a retained earnings balance of $20,000. The company paid a total of $3,000 in dividends and earned a net income of $60,000 this yr. What is the ending retained earnings remainder?

(Effigy)Montana Incorporated began the year with a retained earnings balance of $50,000. The company paid a total of $5,000 in dividends and experienced a net loss of $25,000 this year. What is the ending retained earnings balance?

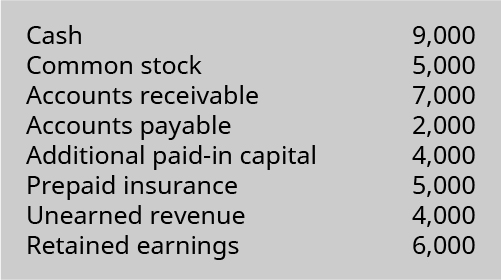

(Figure)Jesse and Bricklayer Fabricating, Inc. general ledger has the following account balances at the end of the twelvemonth:

What is the total ending balance as reported on the company'south Statement of Stockholder's Equity?

(Figure)Roxanne'south Delightful Candies, Inc. began the yr with a retained earnings rest of $45,000. The visitor had a great year and earned a cyberspace income of $eighty,000. However, the company's controller adamant that it had fabricated an fault when calculating depreciation in the preceding year, resulting in an understated depreciation expense corporeality of $2,000. What is the ending retained earnings remainder?

Exercise Set B

(Figure)Birmingham Company has been in business for five years. Last year, it experienced rapid growth and hired a new accountant to oversee the concrete assets and tape acquisitions and depreciation. This yr, the controller discovered that the accounting records were not in order when the new auditor took over, and a $3,000 depreciation entry was omitted resulting in depreciation expense being understated final year. How does the company brand this type of correction and where is it reported?

(Figure)Chelsea Visitor is a sole proprietorship. Ashley, Incorporated is a corporation. Which visitor would report stockholder's equity and retained earnings and not simply owner'south equity? Why? What is the difference between these accounts?

(Figure)Tart Restaurant Holdings, Incorporated began the year with a retained earnings balance of $950,000. The company paid a total of $14,000 in dividends and experienced a net loss of $20,000 this yr. What is the ending retained earnings residuum?

(Effigy)Josue Fabricating, Inc.'southward accountant has the following information available to gear up the Statement of Stockholder's Disinterestedness for the year merely ended.

What is the total residuum on the company's Statement of Stockholder'southward Equity? What is the amount of the contributed capital letter?

(Figure)Trumpet and Trombone Manufacturing, Inc. began the year with a retained earnings remainder of $545,000. The company had a great yr and earned a cyberspace income of $190,000 this yr and paid dividends of $14,000. Additionally, the company'southward controller determined that it had made an fault when calculating tax expense in the preceding year, resulting in an understated expense corporeality of $22,000. What is the ending retained earnings residuum?

Trouble Set up A

(Figure)The board of directors is interested in investing in a new technology. Appropriating existing retained earnings is a selection for funding the new applied science. You are a consultant to the board. How would you explain this option to the board members so that they could make an educated conclusion?

(Figure)You are a consultant for several emerging, loftier-growth technology firms that were started locally and have been a part of a business incubator in your area. These firms start out as sole proprietorships but rapidly realize the need for more capital and oft incorporate. Ane of the common questions y'all are asked is virtually stockholder's disinterestedness. Explain the characteristics and functions of the retained earnings account and how the account is different from contributed capital.

(Effigy)Y'all are the accountant for Kamal Fabricating, Inc. and you oversee the preparation of financial statements for the year just ended 6/xxx/2020. You have the following information from the visitor's general ledger and other fiscal reports (all balances are terminate-of-year except for those noted otherwise:

Prepare the company's Statement of Retained Earnings.

Problem Ready B

(Effigy)You are a CPA working with sole proprietors. Several of your clients are because incorporating considering they demand to expand and grow. I client is curious about how her financial reports volition change. She'due south heard that she may need to prepare a statement of retained earnings and a statement of stockholder's disinterestedness. She's confused about the difference betwixt the two and what they report. How would you explain the characteristics and functions of the ii types of statements?

(Figure)You are a consultant for several emerging, loftier growth technology firms that were started locally and take been a office of a business incubator in your area. These firms start out equally sole proprietorships but chop-chop realize the need for more capital and often contain. One of the common questions you get is about stockholder'southward equity. Explain the primal ways the companies need to view retained earnings if they want to utilise it as a source of capital letter for futurity expansion and growth after incorporating.

(Figure)Y'all are the accountant for Trumpet and Trombone Manufacturing, Inc. and you oversee the preparation of financial statements for the year just concluded 6/30/2020. You accept the following information from the visitor's general ledger and other financial reports (all balances are end-of-year except for those noted otherwise):

Gear up the company's Argument of Retained Earnings

Thought Provokers

(Effigy)Utilise the internet to discover a publicly held company's annual report. Locate the section reporting Stockholder's Equity. Assume that you piece of work for a consulting business firm that has recently taken on this firm as a client, and it is your job to cursory your boss on the financial wellness of the company. Write a brusk memo noting what insights you get together by looking at the Stockholder'southward Equity section of the financial reports.

(Figure)Apply the cyberspace to find a publicly held company'southward almanac report. Locate the section that comments on the Stockholder's Disinterestedness section of the fiscal reports. What additional insights are you able to learn past looking further into the commentary? Is there annihilation that surprised y'all or that yous remember is missing and could help yous if you were deciding whether to invest $100,000 of your savings in this company's stock?

Footnotes

- 1 Cracker Barrel. Cracker Barrel Old State Store Annual Report 2022. September 22, 2022. http://investor.crackerbarrel.com/static-files/c05f90b8-1214-4f50-8508-d9a70301f51f

- 2 Kevin M. LaCroix. "Financial Statements Continue to Reject for U.South. Reporting Companies." The D & O Diary. June 12, 2022. https://www.dandodiary.com/2017/06/manufactures/sox-generally/fiscal-restatements-continue-decline-u-south-reporting-companies/

Glossary

- appropriated retained earnings

- portion of a company'due south retained earnings designated for a particular purpose such as time to come expansion, special projects, or as role of a company's risk management program

- contributed capital

- possessor'due south investment (cash and other assets) in the business organisation, which typically comes in the form of common stock

- deficit in retained earnings

- negative or debit rest

- earned capital

- capital earned by the corporation as role of business operations

- owners' equity

- concern owners' share of the company

- prior menstruum adjustments

- corrections of errors that occurred on previous periods' financial statements

- restatement

- correction of financial statement amounts due to an accounting fault in a prior period

- restricted retained earnings

- portion of a company'due south earnings that has been designated for a particular purpose due to legal or contractual obligations

- argument of stockholders' equity

- provides the changes between the beginning and catastrophe balances of each of the stockholders' disinterestedness accounts during the menstruum

Source: https://opentextbc.ca/principlesofaccountingv1openstax/chapter/compare-and-contrast-owners-equity-versus-retained-earnings/

Posted by: robinsonsciespoins.blogspot.com

0 Response to "Is An Owner's Draw Retained Earnings"

Post a Comment